Market Navigator for the Month Ending February 28, 2026

Market Navigator for the Month Ending February 28, 2026

Presented by Grant Capital

February was a challenging month for stocks, as concerns surrounding the disruptive nature of AI and shifting geopolitical risks weighed on investor sentiment. Domestic equities ended the month in the red; however, bonds and foreign stocks fared better.

1. Beyond the Headlines: Challenging February for Markets

2. Geopolitical Update: Shifting Risks Impact Markets

3. Economic Report Updates: Slowing Growth

4. Looking Ahead: Shifting Risks

Beyond the Headlines: Challenging February for Markets

Markets were mixed in February, driven by rising investor concern surrounding the potentially disruptive nature of AI and shifting geopolitical risks. The S&P 500 fell 0.76 percent in February while the Dow Jones Industrial Average was up 0.31 percent. The technology-heavy Nasdaq Composite Index was down the most, as the index lost 3.33 percent for the month.

These disappointing returns came despite improving fundamentals. Fourth-quarter earnings season is wrapping up, and the results have been impressive. As of February 26, with 95 percent of companies having reported actual earnings, the average earnings growth rate for the S&P 500 was 13.5 percent. This is well above analyst estimates for an 8.4 percent growth rate at the start of earnings season. The better-than-expected results were widespread, as 10 of the 11 sectors saw earnings growth beat expectations. Over the long run, fundamental factors drive market performance, so the continued earnings growth was a positive sign for investors.

While fundamental factors were supportive in February, technical factors were not. All three major U.S. indices ended the month below their respective 200-day moving averages. This marks the first time that all three indices have finished a month below trend since April of last year. The 200-day moving average is a widely monitored technical signal, as prolonged shifts above or below this level can signal shifting investor sentiment for an index.

International stocks continued to outperform domestic stocks in February. Developed and emerging markets both rose during the month, following strong returns throughout 2025 and the start of 2026. The MSCI EAFE Index gained 4.63 percent for the month while the MSCI Emerging Markets Index did even better, up 5.51 percent.

Fixed Income Update: Falling Rates Support Bonds

Bonds were also up in February, as falling long-term interest rates helped support bond prices. The 10-year Treasury yield fell from 4.26 percent at the end of January to 3.93 percent by the end of February. The Bloomberg Aggregate Bond Index gained 1.64 percent in February while the Bloomberg U.S. Corporate High Yield Index gained 0.19 percent.

Bonds were supported by the broader risk-off sentiment, which drove down long-term yields and served as a tailwind for fixed income investors. Rising tensions in the Middle East contributed to the drop in long-term rates, with short-term interest rates largely unchanged. The U.S.-Israel strikes on Iran signaled a further escalation, which could lead to further support for bonds

The Takeaway

· Bond returns were positive in February due to falling long-term interest rates.

· Shifting geopolitical risks could lead to further support for bonds.

Geopolitical Update: Shifting Risks Impact Markets

February served as a good reminder that markets face a variety of risks and that investors should keep that in mind when constructing portfolios. The major news story in February was the joint U.S.-Israeli strikes on Iran at month-end. This was a largely unexpected development for investors that captured global attention and brought further uncertainty to the region. While the initial market reaction to the news was largely muted, the heightened uncertainty could cause further volatility ahead.

Energy prices rose following the strikes, with oil prices rising sharply. If higher energy prices persist, they could serve as a headwind for future economic growth and contribute to rising inflationary pressure. With that being said, a potential de-escalation in the region could cause prices to fall swiftly. For now, we’ll have to wait and see what the ultimate impact of the escalating conflict will have on energy markets.

The Takeaway

· Geopolitical risks shifted in February; however, the initial market reaction was muted.

· Escalating conflicts in the Middle East could contribute to further uncertainty and market volatility.

Economic Report Updates: Slowing Growth

While geopolitical risks garnered headlines and gathered attention at month-end, the economic updates released in February largely showed signs of slower economic growth. The fourth-quarter GDP report showed that the annualized pace of economic growth slowed from 4.4 percent in the third quarter to 1.4 percent in the fourth quarter. The slowdown was partially driven by a slump in federal spending, which in turn was due in part to the shutdown in October. Looking forward, economists largely expect to see growth pick up in 2026; however, if we continue to see slower growth, it would likely serve as a headwind for markets.

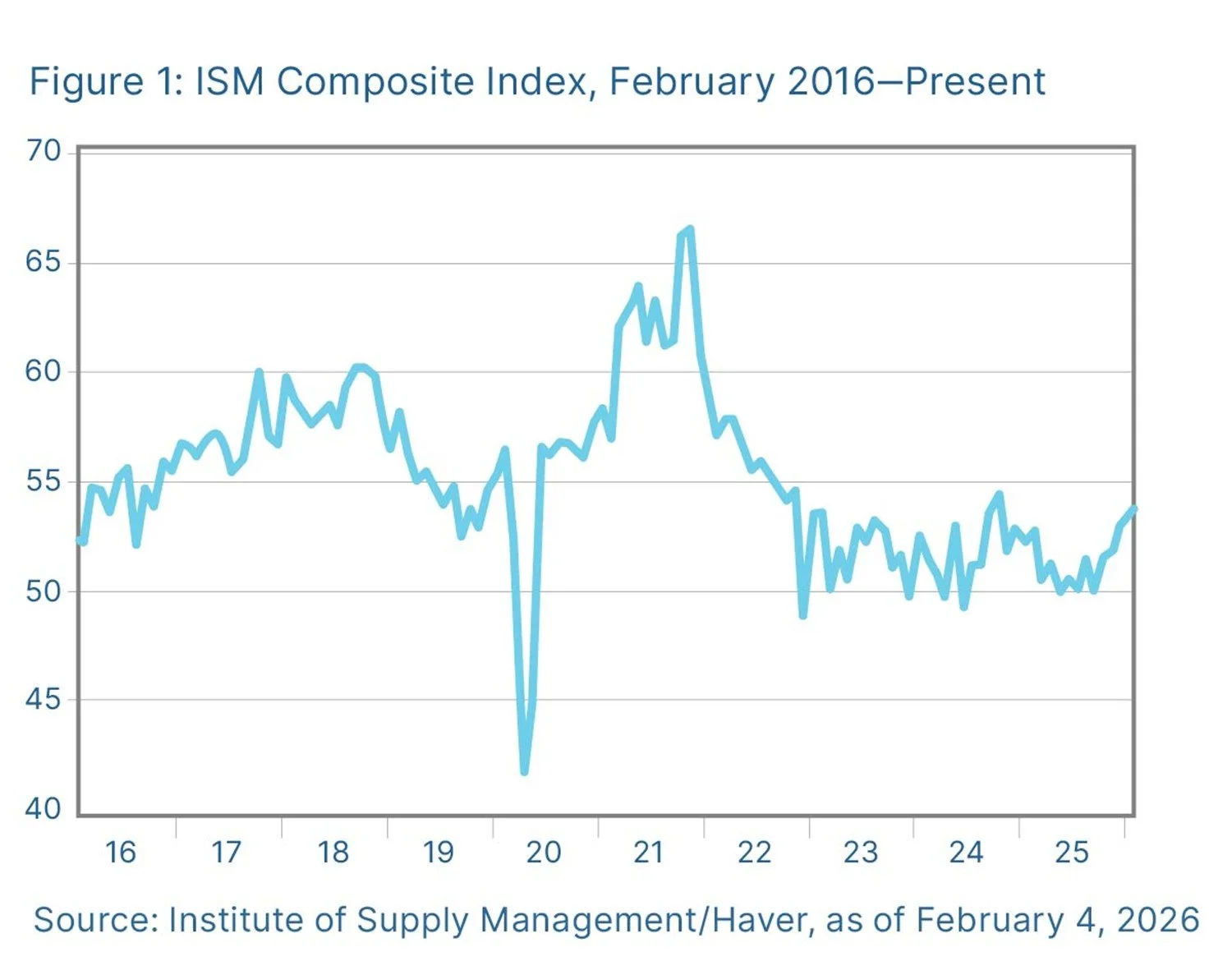

On a more positive note, business and consumer confidence showed signs of improvement during the month. As seen in Figure 1, business confidence, as measured by the ISM Composite Index, hit its highest level in more than a year in January. Manufacturer sentiment, which was a headwind throughout much of 2025, improved notably in January and helped drive the overall improvement for the index. Historically, higher levels of confidence have supported spending growth, so this is a good sign for business investment.

We saw similar improvements for both major measures of consumer confidence during the month. Surveyed consumers cited improved expectations for future economic conditions, which was another good sign for future spending growth. While there’s still work to be done to get consumer confidence back up to recent highs, the improvements in February were encouraging.

The Takeaway

· Economic updates released in February showed signs of slowing growth at the end of 2025.

· Improving business and consumer sentiment should support future spending growth.

Looking Ahead: Shifting Risks

February was characterized by shifting risks for investors. Throughout much of the month, investors were focused on company earnings and the potentially disruptive impact of AI on various industries. By month-end, however, geopolitical risks took center stage. While the initial market reaction to the escalating conflict in the Middle East was largely muted, the increased uncertainty could lead to future volatility and should be monitored.

Aside from geopolitical risks, there are other potential risks that investors should be aware of. The domestic economic backdrop continues to show signs of slowing growth, which could be a headwind for markets later in the year. Additionally, the November midterm elections will be another source of political uncertainty that could negatively impact markets towards year-end.

On the whole, however, things remain solid as we finish out the first quarter. Companies have demonstrated resilient growth despite the shifting risks, as seen by the better-than-expected earnings growth in the fourth quarter. While GDP growth slowed at the end of 2025, it’s important to remember that slower growth is still growth. As long as companies continue to adapt and grow earnings as expected, investors can expect further appreciation over the long run.

While February served as a reminder that risks can shift suddenly for markets, the long-term outlook remains positive due to the solid fundamentals and still supportive economic backdrop. We may face some short-term bumps along the way, but the most likely path forward in our view is for continued economic growth and market appreciation.

Given the potential for further short-term disruptions, a well-diversified portfolio that aligns investor goals and risk tolerance remains the best path forward for most investors. If concerns remain you should speak with your financial advisor to go over your financial plans.

Disclosure: This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent.

###

Grant Capital is located at 7101 College Boulevard, Suite 880, Overland Park, KS 66210 and can be reached at (913) 361-8281. Securities and advisory services offered through Commonwealth Financial Network®, member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services are separate from and not offered through Commonwealth Financial Network®.

Authored by Chris Fasciano, chief market strategist, and Sam Millette, director, fixed income, at Commonwealth Financial Network®.

© 2026 Commonwealth Financial Network®